Renesis Insights

Renesis Team

Not All Crypto Yield Comes From Directional Bets

Some of the most widely used yield-generating strategies in crypto today are not directional bets on Bitcoin or Ethereum. They are market-neutral trades. 25% of crypto hedge funds run market neutral strategies, generating returns through basis trading, funding rate arbitrage, and other DeFi yield strategies. Institutional ETH basis trades alone have generated roughly 9.5% annualized returns from basis spreads, plus an additional 3.5% yield from ETH staking rewards.

Ethena USDe is one such implementation of this strategy at scale. Whenever crypto yield products offer higher returns, comparisons are often made to the UST-Luna collapse, the algorithmic stablecoin that wiped out $40B in a week. That said, Ethena's model is not the same as UST's.

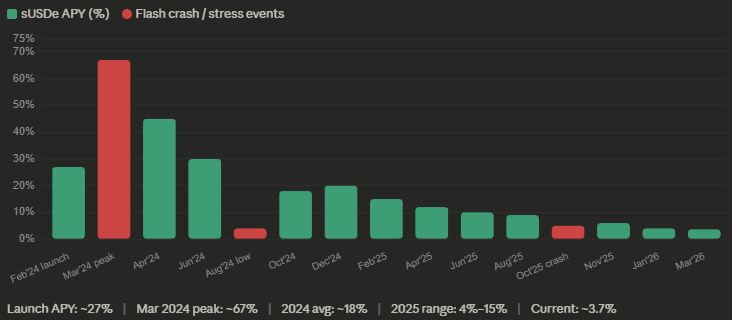

At launch, USDe offered yields of around 27% APY, with rates reaching as high as 67% APY at certain points. As of Q1 2026, Ethena USDe has a circulating supply of approximately $5.92 billion, making it the third-largest stablecoin in existence. Today, USDe's variable DeFi yield ranges between 4% and 15%, with the average APY over the last 7 days at 9.4% and the 90-day average at 11.8%. The yield exists, but it is not fixed. It fluctuates based on market conditions. The sources of this yield and the associated risks need to be fully understood by fund managers allocating capital, particularly what could go wrong.

( Source : Stablecoin Insider )

How Ethena USDe Actually Works

Ethena's foundation is built around a delta neutral strategy. When a user deposits collateral such as stETH, BTC, or ETH, Ethena simultaneously opens an equal size short perpetual futures position on centralised exchanges like Binance, Bybit, and others.

The result is a position that is neutral to price movements. If ETH drops 10%, the collateral loses 10% in value. But the short futures position gains 10% as well. The two cancel each other out. The dollar value stays stable. This is the delta neutral model.

In return for the deposited collateral, the user receives USDe, a synthetic dollar backed by this hedged position. Users can stake USDe to receive sUSDe, which is where the DeFi yield compounds.

Where the Ethena USDe Yield Comes From

There are two engines that are generating yield inside Ethena simultaneously.

1) LST Staking Rewards

A large portion of Ethena’s collateral consists of LSTs such as stETH. These tokens represent ETH that has been staked on the Ethereum network. When ETH is staked, it helps secure Ethereum and in return, validators receive staking rewards from the network. Those rewards are passed through to holders of LSTs like stETH. As a result, they earn 3-4% APY from Ethereum which is stable regardless of market conditions. This is the stable and predictable part of the yield engine.

2) Funding Rate Arbitrage

The second source of yield comes from Ethena's delta neutral hedging strategy and funding rate arbitrage. Ethena opens an equivalent short perpetual futures position for every dollar of ETH or BTC collateral. These short positions participate in perpetual funding system. Every few hours perpetual futures markets exchange funding payments between long and short traders. When markets are bullish, long traders pay short traders. Ethena which is on other side holding large short positions, collect these payments. This is the volatile and market dependent component of the yield.

The 3 Risk Components Inside Every Ethena USDe Position

This is where fund managers need to pay attention. Ethena USDe's DeFi yield does not come from one source. It comes from different sources and that creates distinct risk components.

1) Funding Rate Risk

Since funding rate arbitrage is the major yield source, it is also the major risk. If funding rates stay negative for a long period, Ethena's protocol revenue turns negative. Ethena maintains a reserve fund of $61 million as of March 2026 for this situation, but it is finite. The losses will be absorbed until the reserve is depleted.

A prolonged bear market with negative funding can compress sUSDe yield toward zero. A fund manager holding a USDe position should have an informed view on where funding rates are in this cycle before sizing positions.

2) LST Collateral Risk

A portion of Ethena's backing consists of liquid staking tokens like stETH. These are not always perfectly pegged to ETH. The worst case of this occurred in June 2022, when stETH briefly traded at a 7% discount to ETH during the Terra/Celsius collapse. It did recover within a few months.

Ethena limits this risk through reserve diversification, low leverage, and a custody structure that reduces the probability of a temporary depeg triggering forced liquidations. However, LST basis risk remains a risk component within the system that may not be immediately visible on most dashboards.

3) Exchange Counterparty Risk

Ethena executes its delta neutral strategy through centralised exchanges. Centralised exchanges introduce counterparty risk because the hedges rely on third party trading venues being operational and solvent. The architecture of Ethena addresses this by not depositing collateral on any exchange directly.

Collateral instead sits off-exchange settlement custody via providers like Copper ClearLoop. Additionally, shorts are spread across across multiple venues. Having diversification in venues protects the remaining venues but if a exchange fails, the portion of hedge is affected and at risk. The counterparty risk does exist but is architecturally contained as long as off-exchange custody holds.

The Attribution Problem: What Your Portfolio Management System Is Actually Showing You

The operational takeaway for fund managers holding Ethena USDe is whether your portfolio management system shows protocol-level attribution. If your PMS shows just the holdings and not yield from funding rate arbitrage, funding rate compression, or exchange counterparty exposure across Binance and other CEXs, then it is a major reporting gap.

If funding rates compress over a quarter, a fund manager who cannot attribute DeFi yield by source will not know whether their return is deteriorating until it already has. If stETH spreads widen, they will not see it in their PMS. If one of Ethena's major exchange counterparties has a liquidity event, the risk shows up in the position before the dashboard does.

A protocol-level attribution means being able to see yield from staking rewards, funding rate arbitrage collection, and exchange counterparty exposure by venue separately. As DeFi yield strategies get more advanced, the operational gap between funds who can see inside their positions and funds who cannot becomes a performance gap as well.

At Renesis, we currently track receipt token flows and realised PnL for Ethena USDe positions. Deep protocol-level attribution, including a breakdown of yield by source and the ability to surface the three risk components as separate line items, is actively in development. We already provide this level of attribution for Hyperliquid, Morpho, Enzyme, Lighter, Term Max, and a growing list of DeFi protocols.

Understanding which DeFi yield protocols are safe to allocate to is only half the problem for institutional fund managers. The other half is tracking what those positions are actually doing across onchain markets, CEX venues, and DeFi protocols, and reporting it accurately to LPs.

That is what Renesis is built for. A unified platform for crypto funds that gives you real-time NAV, institutional-grade execution, and the operational infrastructure to run DeFi allocations without duct-taping five tools together.

" height="40px" id="b6zcrI2Wj" width="40.000000141897665px"/></svg>)

" height="40px" id="q3tXZs9hp" width="40px"/></svg>)

" height="40px" id="zrymccGxZ" width="35px"/></svg>)

Built by builders.

For builders.

We're a DeFi-native team shipping fast. No enterprise sales cycles, no bloated pricing. Start free, talk to us when you're ready.

" height="48px" id="otROh8Uzr" width="48px"/></g></svg>)